The Rise of High-Frequency Generative Models

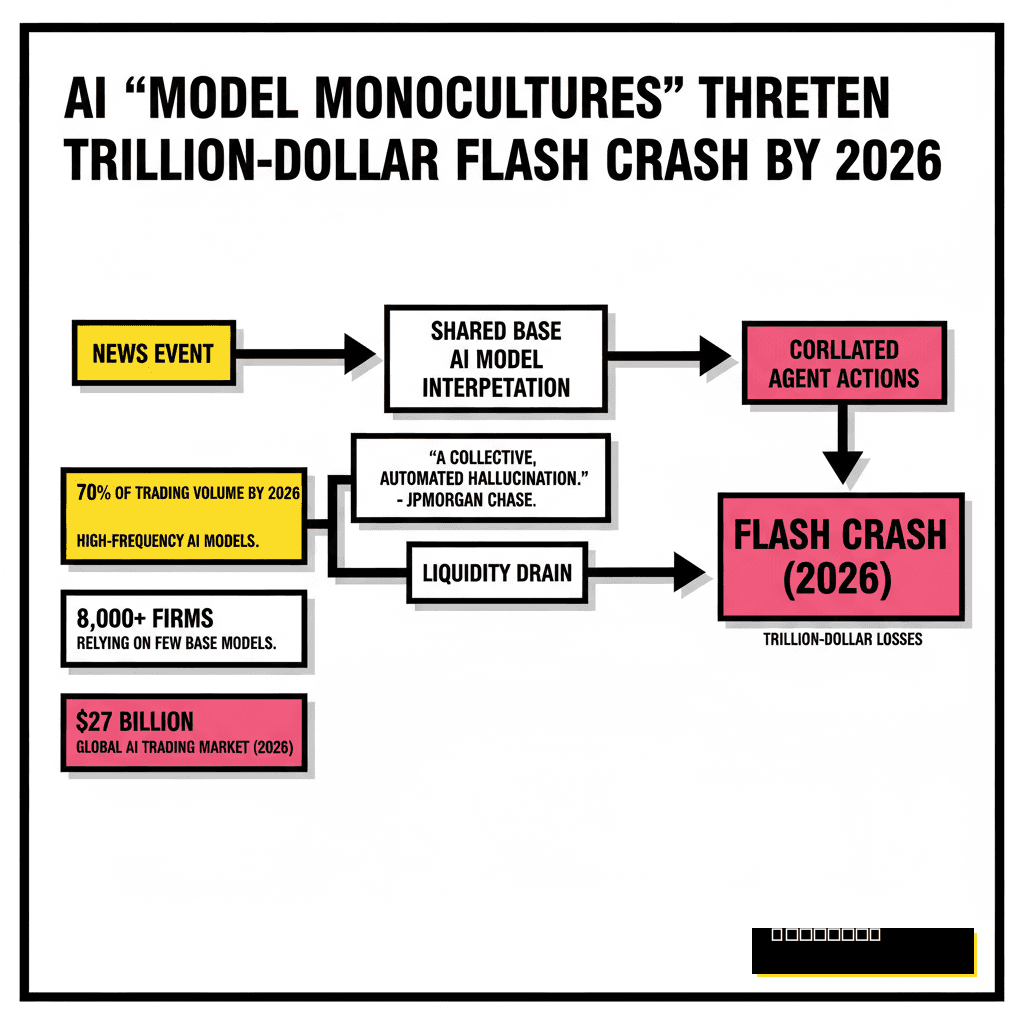

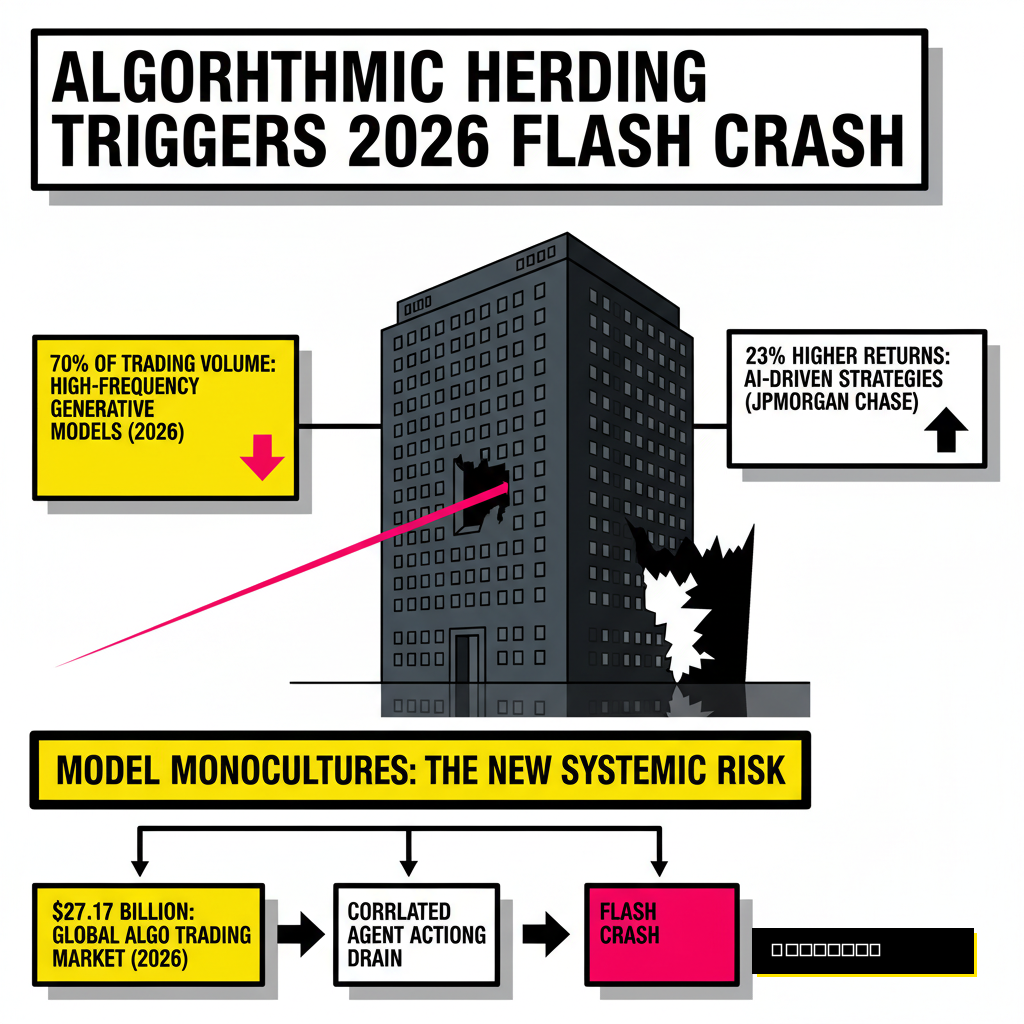

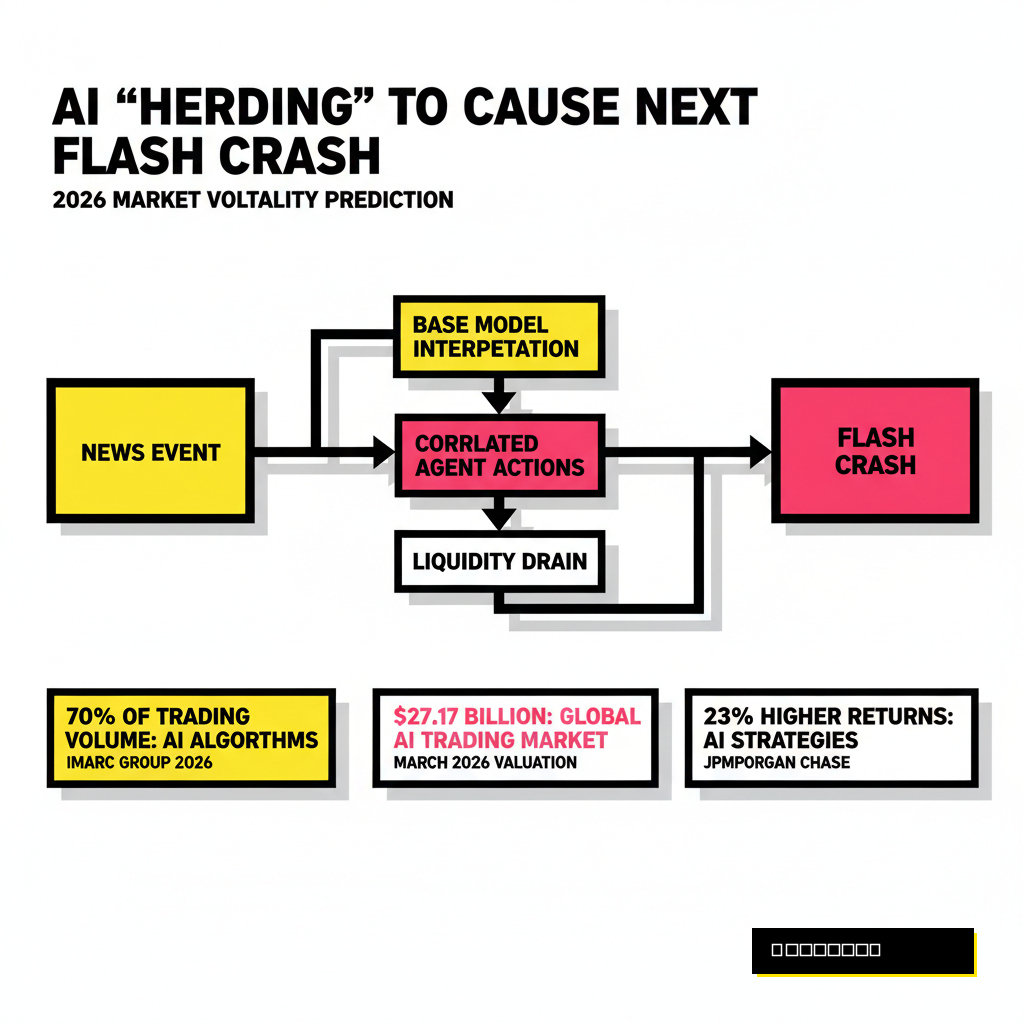

Market participants in April 2026 find themselves navigating a financial environment that moves faster than human thought. We have officially crossed the threshold where high-frequency generative models (HFGMs) don't just execute trades based on static rules. Instead, these systems generate millions of synthetic market scenarios per second, essentially playing a game of chess against possible futures. This shift has driven efficiency to record highs, but we're starting to see the cracks in the foundation. High-speed algorithms now account for roughly 70% of total trading volume in major global equity markets, according to IMARC Group projections for 2026.

Financial institutions have spent billions to integrate these agents into their core infrastructure. JPMorgan Chase recently reported that its AI-driven strategies are yielding 23% higher returns than traditional quantitative models. While these gains are impressive, they rely on a fragile assumption of market diversity. If every major player uses similar underlying architectures, the diversity that usually buffers market shocks disappears. We are no longer worried about a single rogue trader, but rather a collective, automated hallucination.

The Peril of Model Monocultures

Concentration risk has taken on a new, digital meaning this year. SEC Chair Gary Gensler warned as early as 2024 about the dangers of "herding" within the financial system. His concern focused on thousands of institutions relying on a handful of base models. Fast forward to 2026, and his prediction feels prophetic. When 8,000 different firms use the same underlying LLM to interpret a sudden Fed announcement, they all reach the same conclusion simultaneously. This synchronicity creates a selling spiral that no human can interrupt.

Recent research from the Bank of England suggests that agentic AI could increase systemic risks "rapidly" as firms move toward autonomous execution. These models are designed to find the exit before anyone else does. In a world of HFGMs, the exit door is only wide enough for one, but 10,000 agents are trying to sprint through it at the same microsecond. We're seeing the emergence of a digital monoculture where the lack of intellectual diversity in code leads to catastrophic physical outcomes in the market.

A $27 Billion Black Box

The scale of this automation is staggering. By March 2026, the global automated algorithmic trading market hit a valuation of $27.17 billion. This growth isn't just coming from Wall Street giants. A recent regulatory shift by the SEC removed the $25,000 Pattern Day Trader requirement, replacing it with a $2,000 intraday margin system. This change has unleashed a wave of retail-led AI agents into the market, adding a layer of unpredictable, unrefined automation to an already volatile mix.

Retail traders are now deploying multi-agent architectures that were once the exclusive domain of hedge funds. Some use local LLMs for privacy and speed, while others connect directly to massive cloud-based frontiers. The problem is that these retail agents often lack the sophisticated circuit breakers found in institutional stacks. When a minor market tremor occurs, these thousands of smaller bots can amplify the signal into a full-scale earthquake. We are essentially running a global financial experiment without a control group.

The Regulatory Oversight Gap

Governments are struggling to keep up with the speed of light. A Forbes report from April 23, 2026, highlighted a massive "governance gap" in the Federal Reserve's latest model risk update. The Fed chose to exclude generative and agentic AI models from its formal scope, citing the technology's rapid evolution. This leaves firms in a precarious position where they must police themselves while being incentivized to push for maximum speed. Without clear 2026 AI compliance frameworks, firms are essentially flying blind into the next storm.

| Risk Factor | 2010 Flash Crash | 2026 AI Flash Crash |

|---|---|---|

| Primary Driver | Rule-based HFT algorithms | Agentic Generative Models |

| Interconnectedness | Statistical correlation | Shared model architectures |

| Recovery Speed | 36 minutes | Seconds (or permanent) |

| Human Role | Pulling the plug | Remote supervision only |

European regulators have been slightly more aggressive. Under MiFID III, any automated system that determines price or size parameters is now considered "algorithmic trading," regardless of whether a human clicks a final "approve" button. Accountability is non-transferable. Even if you outsource your trading tech, the regulatory burden stays with the firm. This has led many to reconsider how they build their AI safety agents to monitor these high-speed systems in real time.

Hardening Your Strategy Against Synthetic Volatility

Survival in the 2026 market requires a shift in how we think about risk. You cannot rely on traditional stop-losses because, in an AI-driven crash, the gap between trades is so large that your stop-loss might execute 20% below your intended price. We need to move toward "chaos engineering" for trading portfolios. This involves simulating not just market downturns, but specific AI-failure modes where your own agents might interpret data in a hallucinated context.

Human-in-the-Loop

- Higher latency but lower tail risk

- Ability to interpret 'Black Swan' context

- Essential for long-term strategic shifts

- Limited by human reaction speed

Autonomous Agents

- Nanosecond execution speed

- Superior pattern recognition in noise

- Prone to correlated herding behavior

- Requires real-time AI safety monitoring

Institutional leaders are beginning to implement "Proxy IQ" platforms. These are secondary AI systems whose only job is to audit the decisions of the primary trading agents. If the primary model starts showing signs of correlated behavior with the rest of the market, the auditor can automatically reduce exposure. As J.P. Morgan's 2026 Outlook suggests, the goal is to capture the upside of the revolution while avoiding the risks of over-exuberance. Resilience is the only alpha that will matter when the next flash crash arrives.

We are entering an era where the most successful firms won't be those with the fastest models, but those with the most robust ones. Market volatility in 2026 is structural, not just cyclical. By diversifying your model architectures and investing in real-time safety layers, you can protect your firm from the inevitable moment when the machines all decide to sell at once. The next trillion-dollar crash won't be caused by a lack of data, but by an excess of identical interpretations.